Cornerstone Partnership releases nationwide data on effectiveness of shared equity homeownership programs

View the 2014 Sector-wide Social Impact Report

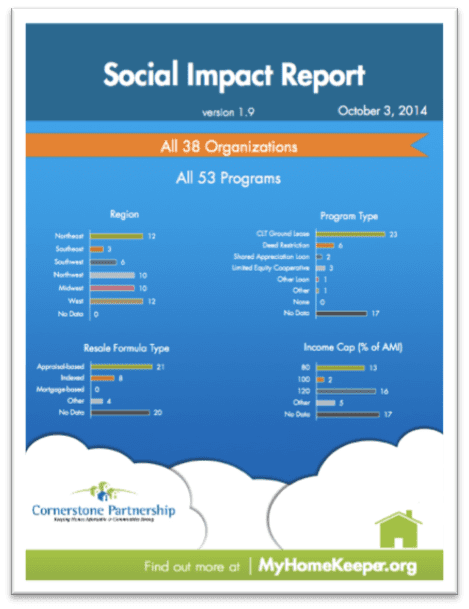

Over the past 5 years, Cornerstone Partnership has been coordinating an ambitious effort to collect key performance data from shared equity homeownership programs across the US, including Community Land Trusts, deed restriction programs, shared appreciation loan programs, and Limited Equity Housing Cooperatives. Today we are releasing the culmination of that work, the HomeKeeper 2014 Sector-Wide Social Impact Report. This report consolidates detailed data from 53 affordable homeownership programs and more than 4,100 home sale transactions involving the investment of $252 million in public subsidy in all regions of the country. It provides the first ever nationwide snapshot of how well affordable homeownership programs are doing at meeting the needs of underserved buyers and preserving affordability of homes as they resell.

The Social Impact Report is a key outcome of Cornerstone’s HomeKeeper project (myHomeKeeper.org). HomeKeeper is a Salesforce.com based software tool that streamlines the job of managing a portfolio of long-term affordable homes. Over 60 organizations are using HomeKeeper to manage nearly 100 different programs. As a byproduct of facilitating the implementation of these programs, HomeKeeper captures key data on program performance. Anonymous transaction-level data rolls up from individual HomeKeeper organizations into the HomeKeeper Hub data warehouse where it provides insight into the social impact that these programs have .

Cornerstone uses the aggregated data in the Hub to produce standardized social impact metrics that were developed with feedback from over 100 experienced practitioners. Each HomeKeeper user receives a confidential report highlighting the social performance of their specific program as well as benchmarking data that allows them to compare their performance to their peers. This benchmarking makes the results more tangible and actionable.

The primary purpose of the social impact data is to help organizations understand their own performance and make ongoing improvements to their programs. The results for each program are confidential so that programs don’t feel pressure to only report successes. But the aggregate data across the whole sector can be shared and, taken together, the results are impressive.

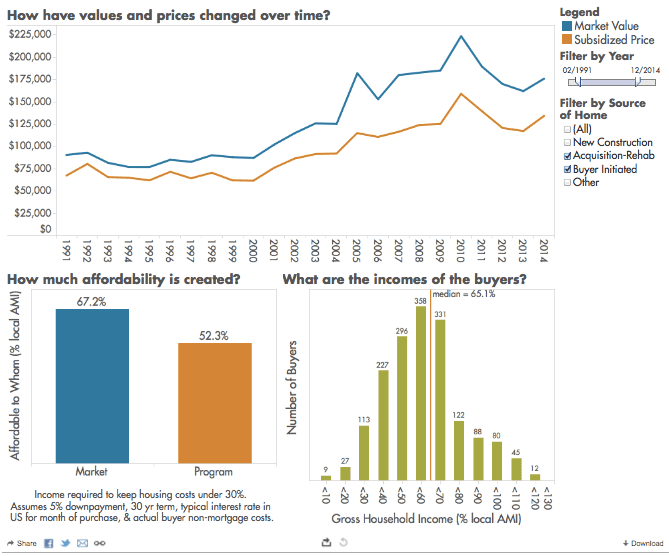

These programs provided largely newly constructed or recently renovated homes to over 4100 low-income families who would otherwise have found homeownership difficult to attain and sustain. They achieved this by investing public and charitable resources and selling the homes for below market prices. The typical home had a value of more than $175,000 on the market but was sold for $115,000 (a 35% discount). This discount meant that overall, homes that would have been affordable to households earning at least 73% of an area’s median income were now affordable to households earning 57% of median income.

Of the families that purchased these homes, nearly 800 have so far chosen to move and resell their affordable homes. These programs ensure that the homes resell to another lower income buyer at an affordable price determined by a shared equity resale formula. The programs each use different formulas and none of the formulas are perfect. Sometimes the homes become less affordable at resale and sometimes they become more affordable. Without comprehensive data over a longer period of time it is hard to evaluate the net effectiveness of these formulas. But this report documents how these programs have succeeded in preserving affordability under diverse local housing conditions and across several market cycles. The typical home was slightly more affordable on resale than it had been when it was initially financed. Preservation of affordability effectively grew the value of public investment in these homes at an annual rate of 4.8%.

At the same time, the families that purchased these affordable homes were able to create significant wealth. The typical family that stayed in their home for 5 years or longer invested just over $2,000 at purchase and received $17,500 at resale, including the $9,000 they paid down on their mortgage and almost $3,000 in profit from their share of appreciation. This represents a 7.97% annual rate of return on the typical downpayment. For most families, the gain alone, excluding the retired mortgage principal, was significantly more than what they could have earned had they invested their downpayment in the stock market. Most sellers (62%) went on to purchase market rate homes with no public assistance.

Homeownership has become a high stakes gamble for lower income families and, for many, it has not always been a good gamble. These programs were all created in hopes of wisely leveraging scarce public resources to offer families a safer and more stable homeownership option and now, for the first time, we have broad national data showing that they are succeeding at that mission.